Roundup Of Cloud Computing Forecasts, 2017

- Cloud computing is projected to increase from $67B in 2015 to $162B in 2020 attaining a compound annual growth rate (CAGR) of 19%.

- Gartner predicts the worldwide public cloud services market will grow 18% in 2017 to $246.8B, up from $209.2B in 2016.

- 74% of Tech Chief Financial Officers (CFOs) say cloud computing will have the most measurable impact on their business in 2017.

Cloud platforms are enabling new, complex business models and orchestrating more globally-based integration networks in 2017 than many analyst and advisory firms predicted. Combined with Cloud Services adoption increasing in the mid-tier and small & medium businesses (SMB), leading researchers including Forrester are adjusting their forecasts upward. The best check of any forecast is revenue. Amazon’s latest quarterly results released two days ago show Amazon Web Services (AWS) attained 43% year-over-year growth, contributing 10% of consolidated revenue and 89% of consolidated operating income.

Additional key takeaways from the roundup include the following:

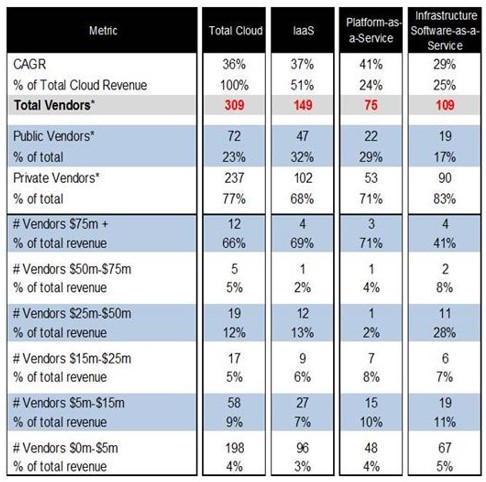

- Wikibon is predicting enterprise cloud spending is growing at a 16% compound annual growth (CAGR) run rate between 2016 and 2026. The research firm also predicts that by 2022, Amazon Web Services (AWS) will reach $43B in revenue, and be 8.2% of all cloud spending. Source: Wikibon report preview: How big can Amazon Web Services get?

Wikibon Worldwide Enterprise IT Projection By Vendor Revenue

- Cloud computing spending is growing at 4.5 times the rate of IT spending since 2009 and is expected to grow at better than 6 times the rate of IT spending from 2015 through 2020. According to IDC, worldwide spending on public cloud computing will increase from $67B in 2015 to $162B in 2020 attaining a 19% CAGR. These and many other fascinating findings are from: The Salesforce Economy: Enabling 1.9 Million New Jobs and $389 Billion in New Revenue Over the Next Five Years, IDC. (PDF, no opt-in).

Rapid Growth of Cloud Computing, 2015–2020

- Gartner predicts the worldwide public cloud services market will grow 18% in 2017 to $246.8B, up from $209.2B in 2016. Infrastructure-as-a-Service (IaaS) is projected to grow 36.8% in 2017 and reach $34.6B. Software-as-a-Service (SaaS) is expected to increase 20.1%, reaching $46.3B in 2017. Source: Gartner Says Worldwide Public Cloud Services Market to Grow 18 Percent in 2017.

Worldwide Public Cloud Services Forecast (Millions of Dollars)

- By the end of 2018, spending on IT-as-a-Service for data centers, software and services will be $547B. Deloitte Global predicts that procurement of IT technologies will accelerate in the next 2.5 years from $361B to $547B. At this pace, IT-as-a-Service will represent more than half of IT spending by the 2021/2022 timeframe. Source: Deloitte Technology, Media and Telecommunications Predictions, 2017 (PDF, 80 pp., no opt-in).

Deloitte IT-as-a-Service Forecast

- Total spending on IT infrastructure products (server, enterprise storage, and Ethernet switches) for deployment in cloud environments will increase 15.3% year over year in 2017 to $41.7B. IDC predicts that public cloud data centers will account for the majority of this spending ( 60.5%) while off-premises private cloud environments will represent 14.9% of spending. On-premises private clouds will account for 62.3% of spending on private cloud IT infrastructure and will grow 13.1% year over year in 2017. Source: Spending on IT Infrastructure for Public Cloud Deployments Will Return to Double-Digit Growth in 2017, According to IDC.

Worldwide Cloud IT Infrastructure Market Forecast

- Platform-as-a-Service (PaaS) adoption is predicted to be the fastest-growing sector of cloud platforms according to KPMG, growing from 32% in 2017 to 56% adoption in 2020. Results from the 2016 Harvey Nash / KPMG CIO Survey indicate that cloud adoption is now mainstream and accelerating as enterprises shift data-intensive operations to the cloud. Source: Journey to the Cloud, The Creative CIO Agenda, KPMG (PDF, no opt-in, 14 pp.)

Cloud investment by type today and in three years

- Amazon Web Services’ (AWS) third quarter revenue was $3.66B, compared to $2.56B during the same period last year, attaining 43% growth. AWS announced that customers had migrated more than 23,000 databases using the AWS Database Migration Service since it became available in 2016. Sources: com Announces First Quarter Sales up 23% to $35.7 Billion. The image is from Amazon’s Q1 2017 Financial Results Conference Call Slides.

AWS Segment Financial Comparison

- In Q1, 2017 AWS generated 10% of consolidated revenue and 89% of consolidated operating income. Net sales increased 23% to $35.7 billion in the first quarter, compared with $29.1 billion in first quarter 2016. Source: Cloud Business Drives Amazon’s Profits.

Comparing AWS’ Revenue and Income Contributions

- RightScale’s 2017 survey found that Microsoft Azure adoption surged from 26% to 43% with AWS adoption increasing from 56% to 59%. Overall Azure adoption grew from 20% to 34% percent of respondents to reduce the AWS lead, with Azure now reaching 60% of the market penetration of AWS. Google also increased adoption from 10% to 15%. AWS continues to lead in public cloud adoption (57% of respondents currently run applications in AWS), this number has stayed flat since both 2016 and 2015. Source: RightScale 2017 State of the Cloud Report (PDF, 38 pp., no opt-in)

Public Cloud Adoption, 2017 versus 2016

- Global Cloud IT market revenue is predicted to increase from $180B in 2015 to $390B in 2020, attaining a Compound Annual Growth Rate (CAGR) of 17%. In the same period, SaaS-based apps are predicted to grow at an 18% CAGR, and IaaS/PaaS is predicted to increase at a 27% CAGR. Source: Bain & Company research brief The Changing Faces of the Cloud (PDF, no opt-in).

60% of IT Market Growth Is Being Driven By The Cloud

- 74% of Tech Chief Financial Officers (CFOs) say cloud computing will have the most measurable impact on their business in 2017. Additional technologies that will have a significant financial impact in 2017 include the Internet of Things, Artificial Intelligence (AI) (16%) and 3D printing and virtual reality (14% each). Source: 2017 BDO Technology Outlook Survey (PDF), no opt-in).

CFOs say cloud investments deliver the greatest measurable impact

- Spending on public cloud computing in Canada will double from $2.3B CAD in 2016 to $5.5 billion CAD in 2020. Overall IT spending will grow from $59B CAD in 2015 to $65B CAD in 2020, by which time IT employment in Canada will surpass 1.2 million jobs. From the end of 2015 to the end of 2020, the adoption of cloud computing will generate more than 50,000 new jobs in Canada. Source: How the Microsoft Ecosystem and Cloud Computing Will Create 110,000 New Jobs in Canada from 2015 to 2020 (PDF, no opt-in).

Cloud investments are fueling new job throughout Canada

- APIs are enabling persona-based user experiences in a diverse base of cloud enterprise As of today there are 17,422 APIs listed on the Programmable Web, with many enterprise cloud apps concentrating on subscription, distributed order management, and pricing workflows. Sources: Bessemer Venture Partners State of the Cloud 2017 and 2017 Is Quickly Becoming The Year Of The API Economy. The following graphic from the latest Bessemer Venture Partners report illustrates how APIs are now the background of enterprise software.

APIs are fueling a revolution in cloud enterprise apps

- By 2018, at least half of IT spending will be Cloud-based, reaching 60% of all IT infrastructure, and 60–70% of all Software, Services, and Technology Spending by 2020. IDC also predicts that by 2018, Cloud will also be the preferred delivery mechanism for analytics. Source: IDC FutureScape: Worldwide Cloud 2016 Predictions; Mastering the Raw Material of Digital Transformation (PDF, no opt-in).

- Public cloud platforms, business services, and applications (software-as-a-service [SaaS]) will grow at a 22% CAGR between 2015 and 2020, reaching $236B. Cloud platform revenues, whose 2020 total of $64B will be 45% higher than Forrester projected two years ago. The much larger cloud application market will also grow faster, with the 2020 total of $155B being 17% higher than their 2014 projection. Source: The Public Cloud Services Market Will Grow Rapidly To $236 Billion In 2020.

- Worldwide Cloud IT Infrastructure Spend Grew 9.2% to $32.6B in 2016. Cloud IT infrastructure sales as a share of overall worldwide IT spending climbed to 37.2% in 4Q16, up from 33.4% a year ago. Cloud IT infrastructure sales grew fastest in Japan at 42.3% year over year in 4Q16. Source: Worldwide Cloud IT Infrastructure Spend Grew 9.2% to $32.6 Billion in 2016, According to IDC.

Additional Resources:

- 451 Research: China and India emerging as cloud computing powerhouses in Asia-Pacific (PDF, no opt-in)

- An Overview of the AWS Cloud Adoption Framework, Version 2, Feb. 2017 (PDF)

- Bessemer Venture Partners State of the Cloud 2017.

- Gartner Says Worldwide Public Cloud Services Market to Grow 17 Percent in 2016

- Health IT and the Cloud, 2017 (infographic, PDF)

- How the Microsoft Ecosystem and Cloud Computing Will Create 110,000 New Jobs in Canada from 2015 to 2020 (PDF, no opt-in)

- Hybrid Cloud: The New Standard for Delivery of Digital Transformation

- IDC’s Latest CloudView Multiclient Study Reveals Attitudes and Strategies of the 58% of Organizations Embracing Cloud

- Journey to the Cloud, The Creative CIO Agenda, KPMG (PDF, no opt-in, 14 pp.)

- RightScale 2017 State of the Cloud Report (PDF, 38 pp., no opt-in)

- Spending on IT Infrastructure for Public Cloud Deployments Will Return to Double-Digit Growth in 2017, According to IDC.

- Survey: 93% of Organizations Use Cloud-based IT Services

- The Forrester Wave™: Global Public Cloud Platforms For Enterprise Developers, Q3 2016 (PDF, 17 pp., no opt-in, courtesy of Microsoft)

- The Salesforce Economy: Enabling 1.9 Million New Jobs and $389 Billion in New Revenue Over the Next Five Years, IDC. (PDF, no opt-in)

- Why Custom Apps Grew $100B In The Last 5 Years

- Worldwide Cloud IT Infrastructure Spend Grows 23.0% to $7.6 Billion in the Third Quarter, According to IDC

- Worldwide Competitive Public Cloud PaaS Forecast, 2015–2019.