Public Cloud Soaring To $331B By 2022 According To Gartner

Gartner is predicting the worldwide public cloud services market will grow from $182.4B in 2018 to $214.3B in 2019, a 17.5% jump in just a year. Photo credit: Getty

- Gartner predicts the worldwide public cloud service market will grow from $182.4B in 2018 to $331.2B in 2022, attaining a compound annual growth rate (CAGR) of 12.6%.

- Spending on Infrastructure-as-a-Service (IaaS) is predicted to increase from $30.5B in 2018 to $38.9B in 2019, growing 27.5% in a year.

- Platform-as-a-Service (PaaS) spending is predicted to grow from $15.6B in 2018 to $19B in 2019, growing 21.8% in a year.

- Business Intelligence, Supply Chain Management, Project and Portfolio Management and Enterprise Resource Planning (ERP) will see the fastest growth in end-user spending on SaaS applications through 2022.

Gartner’s annual forecast of worldwide public cloud service revenue was published last week, and it includes many interesting insights into how the research firm sees the current and future landscape of public cloud computing. Gartner is predicting the worldwide public cloud services market will grow from $182.4B in 2018 to $214.3B in 2019, a 17.5% jump in just a year. By the end of 2019, more than 30% of technology providers’ new software investments will shift from cloud-first to cloud-only, further reducing license-based software spending and increasing subscription-based cloud revenue.

The following graphic compares worldwide public cloud service revenue by segment from 2018 to 2022. Please click on the graphic to expand for easier reading.

Comparing Compound Annual Growth Rates (CAGRs) of worldwide public cloud service revenue segments from 2018 to 2022 reflects IaaS’ anticipated rapid growth. Please click on the graphic to expand for easier reading.

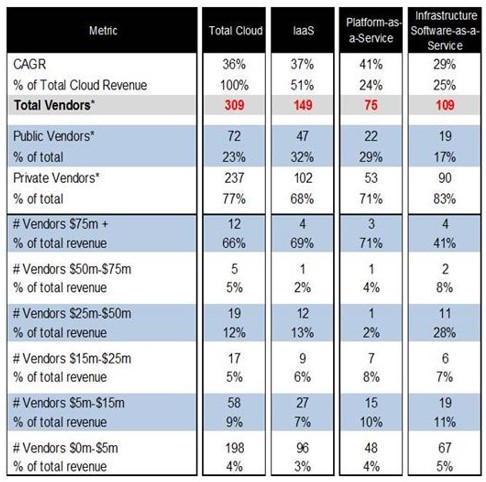

Gartner provided the following data table this week as part of their announcement:

- Business Intelligence, Supply Chain Management, Project and Portfolio Management and Enterprise Resource Planning (ERP) will see the fastest growth in end-user spending on SaaS applications through 2022. Gartner is predicting end-user spending on Business Intelligence SaaS applications will grow by 23.3% between 2017 and 2022. Spending on SaaS-based Supply Chain Management applications will grow by 21.2% between 2017 and 2022. Project and Portfolio Management SaaS-based applications will grow by 20.9% between 2017 and 2022. End-user spending on SaaS ERP systems will grow by 19.2% between 2017 and 2022.

Sources: Gartner Forecasts Worldwide Public Cloud Revenue to Grow 17.5 Percent in 2019 and Forecast: Public Cloud Services, Worldwide, 2016-2022, 4Q18 Update (Gartner client access)